If you are thinking about starting a freelance business, you might want to reconsider establishing a company in your own country. Especially if you already happen to reside here, for example when your spouse is an expat stationed in the Netherlands. More and more freelancers and entrepreneurs decide to found their businesses overseas. Why? Mostly due to the fact that multiple foreign countries offer substantial benefits for business owners, making it very profitable to start a foreign business.

The Netherlands is definitely one of those countries. With a very stable political climate, one of the lowest tax rates in Europe and many benefits that come with being a part of the European Union, you can very safely establish your business here for future success. Best of all: starting a company as a freelancer in the Netherlands is not difficult at all! There are some standard procedures you will have to follow of course. In this article you will find more information about the process.

Can anyone start a business in the Netherlands?

The answer to this question is yes. There are no limitations in terms of nationality. However, if you are residing in a country outside of the EU, the procedure will take a bit more effort and time, since you will need a certain permit in order to be able to stay in the Netherlands legally. This will either be a start-up permit, or a self-employed permit. You can find more info about the whole process of applying for the permits on this page about opening a Dutch company.

What do you need when you decide to register your freelance company?

There are several documents you will need to produce when you start the registration process. These contain necessary information regarding the identity of all people involved, as well as accompanying documents about the business itself, possibly an extensive business plan and also your preferred company name. It is advisable to hire a professional firm to guide you through the whole registration process, because it will substantially shorten the timeframe and probably also the total start-up costs.

You will need to think about the company form you will choose. In the Netherlands there is quite a large amount of legal entities to choose from, ranging from a sole trader business to a holding structure with multiple private limited companies. In general a private limited company is advisable, due to the many benefits and securities this legal entity offers. It is also the most chosen incorporated business form in the Netherlands, not just by Dutch entrepreneurs but also by almost all foreign investors.

Why choose the Netherlands to establish your freelance business?

The Netherlands is an extremely safe and stable country for entrepreneurs and foreign investors, with a very high success rate for most innovative businesses. Some of the benefits for your business you can expect here:

- There are ample amounts of successful Dutch businesses in various sectors, proving strength in innovation and ingenuity

- The EU Single Market makes it possible to freely trade services and goods throughout the entire EU

- You can find both Schiphol and Rotterdam port within driving distance, two world-famous logistical locations connecting you to a worldwide infrastructure

- The costs of starting a (freelance) business are fairly low compared to a lot of other countries

- You will find a well-educated and often bi- or even trilingual workforce in the Netherlands, offering you plenty fantastic candidates to choose from should you feel the need to hire personnel

- The Dutch have access to immense international markets and are part of many trade agreements, which works in your favor as a business owner

The Netherlands will offer you a safe and promising environment to establish and grow your business to success. If you want to know more or would like more information about the procedure of starting a business as a freelancer, you can contact https://businessforimmigrants.nl and ask them all your questions. They can assist you every step of the way and offer many extra services.

It has become pretty clear that Brexit has had various effects on businesses currently situated in the UK. A lot of major companies and organizations are already moving their headquarters elsewhere, in order to stay involved with the EU and all its associated benefits. This also means that many start-ups and investors are looking for alternatives to their original plans of starting a UK business. Are you on the lookout for a suitable new location? Then the Netherlands might just be exactly what you are searching for.

Deal or no deal: the UK is withdrawing

The fact that the UK will soon no longer be part of the EU means that businesses situated in the UK will also feel the consequences. In the case of a deal there might be several agreements to stabilize international relations, but the fact still remains that your business probably won’t benefit from all EU regulations anymore.

When there will be no deal, the whole situation becomes even more severe. Without any mutual agreements, the UK basically stands alone. This will be felt in the business sector on various levels, from international trade to customs affairs. There are many different scenarios and every single one of these possibilities definitely involves some kind of restriction for UK companies. Why? Because you will no longer be seen as an EU-member.

Consequences of your company being ‘cut off’ from the EU

The EU offers many benefits for its member states, which are especially beneficial for entrepreneurs and investors. This includes factors like the single market, healthy competition, substantially reduced paperwork, free movement of people, goods and services, harmonized standards and so on. The EU offers you the possibility to trade in a very large market without customs, import taxes nor a long list of complicated regulations. Once Brexit is finalized, you might lose some (or even all) of these benefits. Suffice to say, this will have a negative impact on the flexibility, adaptability and overall success of your (future) business.

How to avoid this? Move your start-up or business to the Netherlands

You definitely won’t be the first! According to The Guardian, the Dutch government states that more than 250 UK companies have already made the move to Holland. The Netherlands supposedly has gained almost 2000 new jobs due to Brexit.[1] These companies are active in several key industries and sectors, such as the health sector, the creative industry, financial services and the logistics sector.[2] Some well-known names that have already established their headquarters in the Netherlands include Sony and Panasonic, Discovery Channel and Bloomberg.

How to proceed with moving your business to the Netherlands?

If you want to know exactly what your options are, contact us immediately. Intercompany Solutions can assist you every step of the way, whether you already own a company or are planning to start a business in the Netherlands. Don’t miss out on all the benefits Holland has to offer and take action now, while you are still in the position to go through the procedure as an EU-citizen.

[1] O'Carroll, L. (2019, 9 February). Brexit: Netherlands talking to 250 firms about leaving UK. Link: https://www.theguardian.com/politics/2019/feb/09/brexit-uk-companies-discuss-moving-to-netherlands.

[2] Pieters, J. (2019, 25 januari). Over 250 companies considering move to NL over Brexit: report. Link: https://nltimes.nl/2019/01/25/250-companies-considering-move-nl-brexit-report.

It has almost been two years since the infamous Brexit referendum. A small minority of Brits then made it clear, that they no longer wish to be part of the European Union. And so Brexit was born. After many negotiations and struggles there is still no clear view about the road ahead, meaning that the UK may or may not become independent on March 29, 2019.

Intercompany Solutions CEO Bjorn Wagemakers and client Brian Mckenzie are featured by CBC News - Dutch Economy braces for the worst with Brexit, in a visit to our notary public on 12 February 2019.

In either case, there will be consequences for every single party involved. Of course if there is no deal, the situation can become frantic as there will be no agreements with the EU. The UK might find itself in a very uncomfortable position, and not just with the EU but with many other nations that have trade agreements with the EU. In the case of a deal, there are still many factors that will influence business owners and entrepreneurs who work either from the UK or from an EU-member state.

There’s a rather large grey area between deal and no deal, which will have various consequences depending on the scenario playing out. Plus; the financial losses to sustain the whole process up until now have been severe. The big question for everyone is whether the UK will stay involved with the EU at all, and if yes; in what role? The long-term relationship between the UK and Europe is very unstable and this can have massive effects on your business. It doesn’t even matter if that business already exists, or is just an idea at this moment.

From the UK to a business in the Netherlands

In this article we will inform you about the most important details of Brexit and the possible consequences of all scenarios. You will also find information about the benefits of having a business in an EU-member state, and why the Netherlands is possibly one of your best options. Huge companies like Sony, Discovery and Panasonic are already moving their headquarters from the UK to the Netherlands. We will discuss why this is a solid and smart move that might be beneficial for you too.

Start a business in The Netherlands

Why is Brexit bad for business?

The negotiations between Brussels and the UK have been going on for almost two years by now, and still there is no consensus. Major issues like the border between North-Ireland and Ireland are unresolved up to this date. This leaves a huge amount of entrepreneurs, business owners and foreign investors in the dark about the choices they should make. In the case of a deal, which means the UK will not be a member state of the EU any longer but with the inclusion of agreements between both parties, there will be losses in terms of national income. The Financial Times assessed the situation and according to their expertise, the outcome would be as follows:

- If the UK stays a member of the single market: 2% loss

- In the case of a free trade deal with the EU: 5% loss

- If trade between the UK and EU is commenced under WTO rules: 8% loss[1]

Needless to say, that a no-deal situation resulting in a hard Brexit may include financial consequences which will be far more severe. Large corporations and companies have already initiated steps towards damage-limitation. Companies like Bentley were slowly returning to profit but might fail anyway, when a hard Brexit becomes reality. Adrian Hallmark, Bentley’s CEO, explained to The Guardian: “It’s Brexit that’s the killer, if we ended up with a hard Brexit... that would hit us this year because we do have a potential to get beyond break-even to do the turnaround. It would put at fundamental risk our chance of becoming profitable.”

In the eventuality that he would need to stop production in the UK-based Crewe plant, this would cost Bentley millions a day.[2] And Bentley is not the only worried company, which is exactly why many multinationals are swiftly moving their headquarters to ‘safer terrain’ like the Netherlands. Because the benefits and profits of staying within the EU are very real for most business owners.

The repercussions of Brexit: More than 250 companies are considering relocation to Holland

Hundreds of businesses are discussing options for relocation with Holland’s government, as they are worried about their trade on the European market after the British exit from the EU. Several popular companies have declared their firm decisions to relocate.

Consequences for businesses

Brexit and the uncertainty about its specifics strongly motivate companies to leave Great Britain and move to Holland. In 2018 Panasonic announced its intention to move to Amsterdam. More recently Sony also communicated its plan to relocate, citing Brexit as the reason for these developments.

The Dutch Agency for Foreign Investment claims that it has been contacted by more than 250 companies to discuss their relocation to Holland. In 2017 the number was 80, and at the beginning of 2018 it increased to 150.

More businesses are expected to express interest in moving to the country of windmills and tulips before the total figure is announced the following month. A representative of the Dutch Foreign Investment Agency stated that every company’s arrival, regardless of its size, is good news.

The United Kingdom loses and the Netherlands wins?

Britain recently lost a major player in the face of EMA (European Medicines Agency), an institution employing approximately 900 highly qualified workers. EMA has decided to establish in Amsterdam. Other countries are also benefitting from Brexit, because a number of companies in the financial sector plan to move their operations and employees overseas to cities such as Luxembourg, Frankfurt, Paris and Dublin.

It may seem that Holland is benefitting much from Brexit because of the rapidly increasing interest in the country as a destination for business establishment. Still, the companies that actually move will only alleviate the negative consequences of Brexit for Holland. The effects of Brexit are still ambiguous but the country has considered a no-deal situation regarding the rights of British residents.

The European Union in a nutshell

Every member state has accepted the four freedoms of the EU, which are basically the pillars of its existence:

- Free movement of goods

- Free movement of capital

- Free movement of services

- Free movement of people

It is obvious how these freedoms are beneficial for companies based in one of the member states. All companies inside ‘the bloc’ can buy and sell products and services freely within the borders of the EU. To keep the market fair for everyone, a regulatory framework exists that prevents a party from gaining unfair competitive advantages.

Member nations also have the obligation to implement EU law into their own national law and to recognize mutually shared standards. Another important role the EU plays, is that of a common customs union. The member states can trade freely within the borders of the EU, though all non-EU countries are bound to common tariffs on imports. All in all, the EU protects its member states in many ways but also limits countries’ autonomy. This is exactly why the UK decided to leave the EU.

What are the benefits of trading within the EU?

The European single market is obviously the main benefit here. Currently the EU is the largest single trader in the world, accounting for 16.5% of the total sum of imports and exports around the globe.[3] The main goal of the EU is not only the possibility for free trade amongst its members, but also the liberalization of world trade. Some tangible benefits of owning a business in an EU member country such as the Netherlands include:

- No internal trade barriers

- Healthy competition in services

- Reduced overall business costs

- No monopolies or cartels counteracting competition

- Reduced amount of paperwork

- Various harmonized standards

- A more efficient way of doing business

- Free movement of people resulting in a multinational labor force

- A single trade currency – the Euro

This is why being a member of the EU has offered key benefits to UK businesses. The EU includes some of the wealthiest and most prosperous countries worldwide, offering every business owner access to an enormous amount of suppliers. You can basically see the EU like a big marketplace, which offers an amount of convenience similar to doing business in your own country. No customs, no import taxes and a lot less regulations to slow trade down.

Fair and open trade possibilities

The World Trade Organization ensures that obligations and trade agreements between countries worldwide are transparent and fair. All EU regulation and trade policy is made on behalf of the EU by the Commission, who work closely within the framework of the WTO in order to ensure fairness and openness. The commission also works very closely with national governments, the European Parliament and global organizations to be able to adapt quickly to necessary worldwide and local situations and changes.

Because the EU has an extensive network of worldwide trade relations, favorable agreements can be negotiated. This is something a country on its own would not be capable of. All these partnerships are aimed at creating and maintaining a stable and fair single market that provides business owners with many benefits. It also makes it safer for business owners to trade outside of the EU, being protected by numerous multilateral agreements.

The EU provides safety and stable conditions

Next to creating opportunities for business owners, the EU also strives for better working conditions in poorer countries. The EU trade policy is aimed at reducing and putting a stop to malpractices such as child labor, the use of harsh chemicals and creating environmental hazards as well as combating price volatility. Countries in distress can be actively pushed forward by actions such as temporarily lowering duties, providing governance advice and supporting smaller national businesses. By choosing to establish a company in the EU, you automatically choose safe conditions.

Is a company in the Netherlands a good Brexit alternative for your business?

In general, starting a Dutch business is almost always beneficial due to the large amount of benefits and possibilities the Netherlands has to offer. If you’re still in doubt though, you can ask yourself a few questions first. The answers will determine whether Holland is a good place to start your company:

- What kind of business are you planning to establish?

- Is it possible for you to start such a company in the Netherlands?

- Is there a fitting niche for the services or products you want to offer?

- Would your company be competitive in certain ways?

- Will it be easier for you to trade with a business based in the Netherlands, or would this entail certain financial benefits you currently miss out on?

It’s a wise to answer these questions for yourself beforehand, since you might need to answer them once you decide to start the process of establishing a Dutch business. If you already own a successful UK business but want to move it to the Netherlands, you might also have to explain how your company will be beneficial for the Dutch economy.

''The Netherlands to become the centre for financial trading infrastructure of the EU27

The AFM conducted more than 150 interviews with companies that are interested in applying for a licence. ‘We assume that between thirty to forty percent of the European trade in financial instruments will opt for the Netherlands as a location. Thus, the Netherlands will become the financial trading centre within the EU27’, according to Merel van Vroonhoven, Chair of the AFM. ‘The arrival of these parties will also attract other service providers. Moreover, it strengthens the access of Dutch pension funds and other portfolio managers to the capital market’. '' [4]

How can setting up a Dutch business benefit you?

If you have already been thinking about starting or moving your business, the Netherlands proves to be a fantastic choice for almost every single investor or start-up. A business in the Netherlands offers a wide amount of perks and benefits to foreign entrepreneurs. The Dutch have been ranked 4th on the Global Competitiveness Index of the World Economic Forum, the 3rd best country in the world for business by Forbes Magazine due to the profitable business conditions.

A few very good reasons to start a Dutch business:

- One of the lowest tax rates in Europe: between 16.5% and 25% (15-21% from 2021)

- You don’t pay value added tax (VAT) for transactions within the EU

- The Netherlands has the largest number of treaties worldwide for double tax avoidance

- The Dutch have a solid reputation in global (e-)commerce

- More than 90% of the population speaks English and in most cases a second foreign language

- The Dutch labor force is highly educated and ranks 3rd in the global top

- The Dutch offer an innovative international business atmosphere

- Foreign entrepreneurs and investors will profit from a stable legal and political climate and a plethora of outstanding international relations

The procedure for starting a Dutch business

If you want to be able to enjoy all the benefits the Netherlands has to offer, you will need to follow a certain procedure to establish your company here. This is where Intercompany Solutions comes into the picture. We can help you set up a Dutch business in just a few working days. We can also assist you to transfer your current business to the Netherlands. Our procedure consists of 3 general action steps:

Step 1

You will be asked to send in all the necessary documentation as well as proof of your identity, which we will check thoroughly. If you already have a company name in mind, we will check the availability of that name during this stage too.

Step 2

After all the checks we prepare all the documentation that will be needed to register your company. When these documents are finished, we send them over for you (and possible other shareholders) to sign. Once signed, you send everything back to us so we can start the registration process.

Step 3

With all the signed documents we go to a notary public, who will sign the deed of incorporation and submit the deed of formation to the Chamber of Commerce. You will then receive your registration number as well as your VAT number. Your company officially exists! If you wish, we can also take care of other matters such as applying for a Dutch bank account.

Contact Intercompany Solutions for more information

Intercompany Solutions has many years of experience in setting up businesses for foreigners, as well as handling a great many cases. We can help you with any question you might have related to starting a business in the Netherlands. From the permit you will need to finding the best Dutch bank for your business. Simply contact us for more information, and we will get back to you as soon as possible.

[1] Strauss, D. (2018, 9 October). Brexit explainer: what’s at stake for EU single market and customs union. Link: https://www.ft.com/content/1688d0e4-15ef-11e6-b197-a4af20d5575e.

[2] Neate, R. (2019, 23 January). Companies press Brexit panic button in further blow to Theresa May. Link: https://www.theguardian.com/technology/2019/jan/22/no-deal-brexit-panic-grips-major-uk-firms.

[3] European Union. (2018, 13 November). Trade | European Union. Link: https://europa.eu/european-union/topics/trade_en.

[4] Dutch Authority for the Financial Markets (AFM) (2018, 29 October) The Netherlands to become the centre of European financial trading post Brexit. Link: https://www.afm.nl/en/professionals/nieuws/2018/okt/trendzicht-2019

Updated 11-12-2019

In Holland, a joint venture is an agreement between at least two companies to unite resources in order to pursue a common commercial goal. Each company keeps its identity and carries liability for the losses and profits of the venture.

The investors involved in the creation of a Dutch joint venture first have to establish two companies in the Netherlands. Joint ventures are not specifically regulated for business arrangements of this type. Still, the companies forming the venture must comply with the national corporate law.

Our Dutch agents in company formation can assist you in forming a suitable joint venture meeting the current provisions for corporate control and management.

Joint Venture formation in Holland

A joint venture formed in Holland can be either corporate (between public or private companies or cooperatives) or contractual (of partnerships, limited or not). A corporate joint venture is formed between corporate entities that are legal persons (in contrast to partnerships) and therefore the companies must follow the Dutch Corporate Law. This important factor differentiates corporate from contractual joint ventures.

In Holland, companies and partnerships are subject to different requirements for annual financial reporting and accounting. Our agents in company formation can provide you with comprehensive information on this subject.

Requirements for joint venture establishment in Holland

All incorporated Dutch companies must undergo registration at the National Chamber of Commerce. Any joint venture performing commercial activities has to be formed by registered entities. In particular cases, joint ventures can be subject to the Dutch Act on Competition. On the other hand, contractual ventures must meet the requirements of the national contract law.

Holland has not enforced any commercial restrictions on joint ventures and they can be established in any area of business. This establishment type is not required to comply with specific duration. Still, if the entities forming a joint venture are meant to exist for a certain time period, then the same period will be valid for the joint venture.

If you need information on other legal entities or you want to incorporate a Dutch company, please, get in touch with our specialists in company formation.

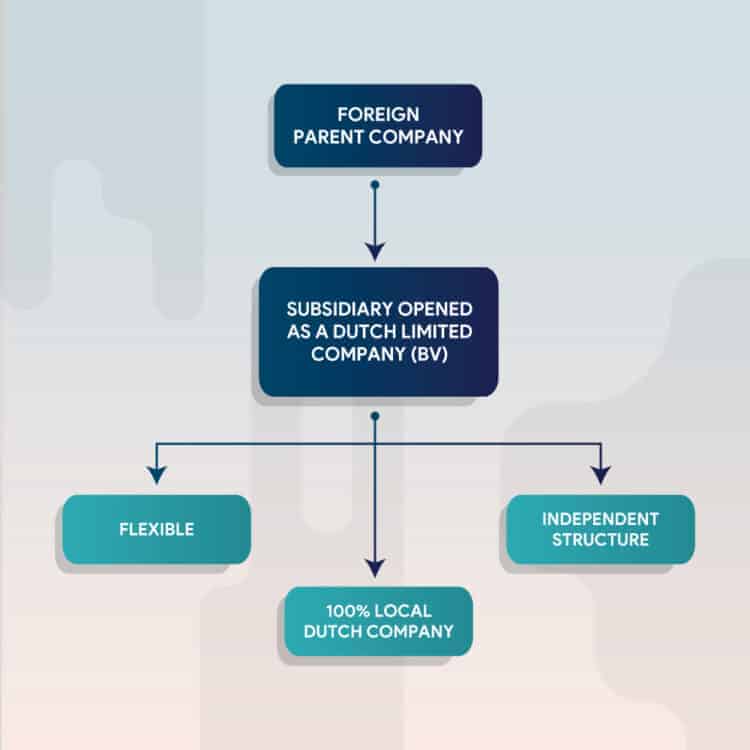

International companies that do not reside in Holland can advertise their business interests and establish a presence in the country by opening a representative (liaison) office. According to the national law liaison offices are not classified as legal entities, since they do not function and exist independently; they are fully subordinated to and dependent on the international corporations that have established them in Holland.

Generally, international companies are interested in settling liaison offices in Holland for the purposes of marketing research: to introduce and promote products on the local market and sign contracts with resident business partners.

Activities of the local liaison office

Being fully dependent and subordinated to the international company that opened it, the Dutch liaison office cannot perform its own activities (it cannot manufacture goods or provide services). It can, however, support different operations of its parent corporation, e.g. commercial activities (advertisement, promotion and marketing). The Dutch liaison office can also collect information for the purposes of scientific research and similar activities that are auxiliary to the international company.

Dutch liaison offices often serve as intermediaries between their international parent companies and commercial partners in Holland, thus representing the parent companies (acting in their name/on their behalf).

Representative offices cannot generate profit, so international investors willing to establish their products and services on the Dutch market may opt for opening branches instead. Branches are also highly dependent on their parent companies but, in contrast to liaison offices, they can carry out actual business activities.

Dutch liaison office registration

Dutch liaison offices do not need to undergo registration at the National Commercial Chamber. They are considered as structures that simply collect and provide information/provide administrative services to their parent companies without involving any commercial activities. Therefore liaison offices are not taxed in Holland. (Read more on Dutch taxes).

Still, a Dutch liaison office can employ staff and, if so, it has to be registered with the appropriate local authorities for personal income tax. The non-resident individual acting as a Dutch liaison officer and representing the international company needs to apply for residence and work permits.

The Value Added Tax incurred by Dutch liaison offices may be refunded under particular conditions. A Dutch liaison office can receive a refund if its international parent company files regular requests with the local tax authorities.

The Dutch liaison office represents an initial step for international entrepreneurs planning to establish themselves on the market in Holland. At a later point the office may become a branch, if the entrepreneur makes a decision to broaden the range of his local operations.

If you need more information about Dutch liaison offices, please, contact our agents in company incorporation. They will answer your questions about setting up a Dutch business and can represent you in front of the respective authorities.

The present article considers the steps leading to company mergers or acquisitions in Holland. One such step is an investigation called “due diligence” (or DD). It aims to elucidate the actual state of the respective company. DD allows for the assessment of potential risks with the aim to inform the final decision about the transaction and also to adjust the purchase conditions.

Agreement of confidentiality / non-disclosure

During the negotiation phase of merger and acquisition the parties often sign an agreement of confidentiality (non-disclosure), so that any confidential information shared with respect to the tentative purchase remains secret. In this way, the vendor reduces the risk of public disclosure of the supplied information. To minimize the risk further, sometimes penalty clauses are included in the agreement.

Declaration of intent (DoI)

After the agreement of confidentiality has been signed, the (eventual) purchaser has completed due diligence and the initial negotiations have been closed, the parties prepare a declaration of intent (DoI) that provides the conditions for further negotiations regarding the company’s acquisition. The DoI generally contains the following (the list is not exhaustive):

- that preliminary negotiations on company takeover are held between the parties;

- if the negotiations are exclusive (with exact exclusivity period);

- what conditions allow the parties to stop the negotiations;

- latest date for finalization of the acquisition;

- the conditions that need to be fulfilled (in the general case – completed due diligence) in order for the parties to proceed to the next acquisition phase.

Due diligence

During the second phase the purchaser performs an audit called due diligence examination (“DD”). This is an investigation intended to elucidate the state of the respective company and the possible risks, thus allowing the purchaser to make an informed decision on the potential transaction. The DD results are usually reflected in the conclusive purchase agreement terms and also in the statements and guarantees of the seller.

The following (non-comprehensive) list presents some common subjects to DD investigations:

- Human resources / contracts (for labour);

- real estate / contracts for tenancy;

- potential and current legal proceeding;

- rights to intellectual property and licenses;

- (civil) claims;

- insurance matters;

- finance;

- tax.

These details are key to assessing the company and setting its purchase price. They can serve as a basis for indemnities and guarantees in the agreement for purchase. In addition to the legal DD investigation, it is important to perform financial and fiscal (tax) DD examinations.

Vendor DD

Every so often vendors also carry out their own DD investigations (or vendor DD) even before the start of the negotiations for takeover. Company problems can be fixed in time to prevent unpleasant surprises in the process of negotiation.

Agreement of purchase

After the DD examination is completed and the results are in, the parties start negotiating on the provisions of the purchase contract. This contract includes clauses on the risks related to uncertain events, financial and other, and their distribution among the parties. If, for instance, the DD examination has shown that claims are expected from pension funds or tax authorities, the purchaser can request specific guarantees or warranties from the seller (or a change in the price of purchase).

Agreement of share/asset purchase

Company acquisition usually involves a share transaction. The purchaser acquires the company shares held by the vendor by means of an agreement on share purchase. Sometimes it is necessary to conclude a different form of transaction, e.g. if the company to be acquired is a general partnership or a sole proprietor, rather than a legal person. In such cases the companies are subject to transfer of liabilities and assets by virtue of agreements of asset purchase.

Signing the agreement of share or asset purchase

After the parties agree on the transaction conditions (incl. the legal transfer date and the basis of the transaction), they sign an agreement of share or asset purchase (or another form of agreement, such as a merger contract). This phase is often referred to as “signing”. Usually the legal title transfer takes place weeks or even months later for a number of reasons, e.g. to give the purchaser enough time to fund the transaction. Agreements of share or asset purchase can also include resolutive or necessary conditions that must be met and can specify the period before title transfer.

Concluding the transaction

The transaction is concluded after all the necessary papers have been prepared and all requirements therein have been fulfilled or have expired. Then the documents related to the transfer are signed and, if a share purchase is taking place, the actual shares are transferred. Most commonly transfers take place against purchase price payment (or a part of it, if there is an earnout provision). In the Netherlands transfers of company shares are performed via transfer deeds prepared by Latin notaries.

If you are interested in buying or selling company shares for a company acquisition, find our articles below:

The Private Limited Company (BV in Dutch) holding structure saves money and mitigates business-related risks.

As a minimum, the holding structure includes two companies: one is the active company performing business operations, and the other is a personal company holding shares issued by the active company. The law does not differentiate between BVs with respect to their function, therefore the terms “Active BV” and “Holding BV” have no legal meaning.

What is the general structure of a BV holding?

Two Dutch BVs are incorporated using the services of a notary. The first BV performs the business operations of the structure (Active BV). The second BV is a holding company which remains mostly inactive (Holding BV). The owner of the business holds all shares issued by the Holding which, in turn, holds the Active BV’s shares. Our explainer video explains different aspects of the Dutch BV and the Holding structure.

If two shareholders (SH 1 and SH 2) plan to set up a single active company and to hold equal amounts of its shares, the usual scenario is the following: One active BV performing real business operations is incorporated using the services of a notary. Then two holding companies are incorporated above the active company. Both of them own 50% of the active BV. Holding 1 is fully owned by SH 1, while Holding 2 is fully owned by SH 2.

Advantages of the holding structure

The Dutch holding offers two main advantages to entrepreneurs with respect to their business: lower tax burden and decreased business risk. Holding structures may provide tax advantages. The main benefit is the Dutch participation exemption (“deelnemingsvrijstelling” in Dutch).

For instance profits generated by selling the active company and transferred to the holding company are exempt from profit tax. Also, operating from a local holding structure involves a lower risk. The holding BV serves the function of an additional layer between the owner of the business and the actual business activity. Your holding structure can be set up to protect the equity of the company. You can accumulate pension provisions and profits safeguarded from business risks.

How to know if a Dutch holding structure is suitable for your company?

Most tax advisors in the Netherlands would say that setting up just one private limited company is never enough. The incorporation of a holding where the owner of the business is the shareholder is usually more beneficial in comparison to a single BV. In particular situations we certainly recommend setting up a holding, e.g. in case your industry involves higher business risks. The holding BV provides an additional layer of protection between you as the business owner and your actual business activities.

Another valid reason to open a holding is if you are intending to sell the company at some future point. The profits from selling the business will be transferred free of tax to the holding BV thanks to the participation exemption or “deelnemingsvrijstelling” (described in more detail below).

Practical advantage of the holding structure

When you sell (partially or entirely) the shares issued by your Active BV, the profits from the sale are transferred to the Holding BV. Holding companies do not pay taxes on realized profits from selling shares issued by Active BVs. The resources accumulated by the holding can be used for reinvestment in another business or retirement benefits.

If you own shares of the active company, but you have not yet established a holding, you will need to pay from 15 to 25,8% corporate tax with respect to the profit in 2022.

Profits taxation

2020: 16.5% below €200.000, 25% above

2021: 15% below €245.000, 25% above

2022 15% below €395.000, 25% above

In case your holding owns shares in multiple private limited companies, you don’t need to pay off a wage from each stake. This saves money from income tax, administrative procedures and fees. If the holding owns ≥95% of the active BV’s shares, the two private limited companies can file a request to be treated as a single fiscal unit by the Tax Administration.

This allows you to easily settle expenditures between the two companies and gives you an advantage with respect to the annual tax liabilities. The active company (subsidiary) and the holding (parent company) are considered as one taxpayer and therefore you are obliged to submit one tax return for two private limited companies. By keeping shares and profit reserves (including real estate, pensions savings, company cars) in a holding, you are protected from losing accumulated gains if the active company goes bankrupt.

Participation exemption (deelnemingsvrijstelling)

Both the holding and the active limited companies need to pay income tax. Still, double taxation of profit is avoided thanks to the so called participation exemption. According to this measure profits/dividends of the active business can be transferred to the holding free of taxes on corporate income and dividends. The main condition that needs to be met in order for this measure to take effect is that ≥5% of the active company’s shares are owned by the holding. Our specialists can support you throughout the process of company establishment. Please, contact us, to receive guidance and further information.

The present article describes the legal and tax aspects and some practical matters concerning office establishment in Holland. It summarizes information about the Dutch legal and tax system relevant to the required procedures. The article also presents Holland as an international centre of commerce and highlights the location advantages gained by opening a Dutch office. Finally, it discusses other matters of practical importance such as living and labour costs.

Please, do not hesitate to call our tax and incorporation agents if you have legal or tax issues or in case you need any additional information.

Tax aspects of establishing a Dutch office

Company establishment in Holland has numerous tax advantages. Many entrepreneurs choose to incorporate an international structure under an efficient tax regime such as the one in Holland. Dutch legal entities within company structures bring many tax benefits. The main advantages can be summarized as follows:

1) The benefit of double tax avoidance thanks to agreements concluded by Holland and to the EU directives on direct tax;

2) The participation exemption;

3) The option to negotiate agreements with the national tax authorities regarding advance pricing (APAs) and tax ruling (ATRs). Such agreements provide certainty about future tax payments;

4) Holland’s bilateral treaties on investments (BITs)

5) Dutch tax credits for income from foreign sources;

6) The Innovation Box (IB) regime for R&D activities;

7) No withholding tax levied on outbound royalty and interest payments; and

8) The scheme for highly qualified migrants (30 percent ruling).

These tax benefits will be explained in detail below.

Benefits of Dutch holdings

A Dutch holding can serve as an investment centre for companies established in various countries worldwide. Holland is recognized for its favourable regime with respect to holdings, particularly thanks to the participation exemption, coupled with an extensive network of tax treaties and bilateral agreements on investments. The main benefits prompting international businesses to use Dutch holdings as intermediaries are the lower withholding tax in the country where profit is generated, the untaxed receipt of funds accumulated by foreign subsidiaries and the protected status of these subsidiaries. These advantages will be clarified below.

The Government of the Netherlands has declared its general intention to keep and preserve these benefits, considered figuratively as jewels in the crown of the national tax system, regardless of the attempts of the Organisation for Economic Co-operation and Development and the European Union to combat tax avoidance strategies aimed at shifting profits from higher- to lower-tax jurisdictions.

The participation exemption in the Netherlands

As already mentioned, Holland is popular with the so-called participation exemption. If particular conditions are fulfilled, capital gains and dividends obtained from qualifying subsidiaries are not subject to Dutch corporate tax.

This exemption applies if an eligible subsidiary holds no less than 5 percent of the company’s shares. One eligibility criterion is that subsidiaries must not hold the shares with the sole purpose of passive investment in a portfolio. However, even in cases where this purpose is predominant, the exemption still applies if the subsidiaries are paying profit tax of no less than 10 percent (under the rules of tax accounting in the Netherlands) or if less than half of their assets are allocated to passive investments. When the exemption cannot be applied, companies usually have the option for tax credit.

The system for tax ruling in the Netherlands (Advance Pricing Agreements, APAs and Advance Tax Rulings, ATRs)

The Dutch system for advance tax ruling provides clearance in advance by concluding APAs and ATRs with Dutch companies with respect to their tax position. The conclusion of such agreements is voluntary. In general, companies use the system for tax ruling to become aware in advance about the tax liabilities relating to planned intercompany transactions. ATRs provide advance certainty with respect to the tax repercussions of envisaged transactions by clarifying, for example, if they will be eligible for participation exemption. APAs, on the other hand, define when the arm’s length principle can be applied to international transactions between associated companies or different parts of the same company.

Bilateral treaties on investments (BITs)

When investing in a foreign country, one should consider both the respective taxes and the protection of the so-called bilateral treaties on investments, especially if the investments are made in a country with a serious risk profile.

BITs are concluded between two countries to establish the terms for protection of entities from one country investing in the other country. These treaties ensure reciprocal protection and promotion of investments. They secure and protect the investments of entities residing in one of the contracting parties on the other party’s territory. Therefore BITs represent institutional safeguards with respect to foreign investments. Also many BITs provide for alternative mechanisms for dispute resolution where investors whose rights have been infringed upon can opt for international arbitration rather than sue the defaulting country in its courts.

Holland has developed a large network of such bilateral treaties offering investors the best possible security and protection in foreign contracting countries. It is worth to mention that Holland has entered into BITs with approximately 100 states.

Investors who reside in a country signatory can benefit from the protection of its BITs. Therefore Holland is an attractive jurisdiction for setting up holding companies not only due to its favourable tax regime, but also thanks to the numerous BITs it has concluded.

The double tax avoidance decree

In order to encourage Dutch investments into other, especially developing, countries, the Government has introduced a regulation providing a mechanism to lower Dutch corporate tax on profits obtained from investments in countries that have not concluded tax treaties with Holland. This piece of legislation is the Unilateral Double Tax Avoidance Decree (hereinafter referred to as DTAD). As a result of the DTAD the Dutch taxes levied on investments in countries that have not concluded tax treaties with the Netherlands are usually the same as the taxes levied on investments in tax treaty states.

The Innovation Box (IB) regime

Holland boasts a favourable tax climate under the innovation box regime, with regards to companies working in the field of research & development (R&D). Any company generating income from its own developed and patented intangible fixed assets (excluding trademarks and logos) or from assets derived from R&D activities (verified by an official statement) has the option to report the income using the IB regime. Then its eligible income exceeding the costs for the development of the intangible fixed assets will be subject to only 5 percent tax. Any losses associated with the eligible assets can be deducted against the usual corporate tax rate, i.e. 25 percent. If losses are included in the tax return, then they need to be recaptured using the normal rate. Only then the reduced 5 percent rate will become available again.

No withholding tax with respect to royalty and interest payments

Holland is an attractive jurisdiction for setting up (group) license and finance companies. The greatest advantage of establishing a Dutch license or finance company lies in the tax-effective setup of these entities. In broad terms this efficiency stems from the convenient tax treaties that Holland has concluded, coupled with the lack of withholding tax with respect to outbound royalty and interest payments. If certain requirements are fulfilled, these prerequisites allow for an extremely tax-efficient “flow” of license income and finances through the entity in the Netherlands to the eventual recipient.

The scheme for highly skilled migrants

Foreign employees living and working in Holland can benefit from a concession if they meet particular requirements. This concession is called the 30% ruling. According to it, 30 percent of the wages of the international employee remain untaxed. As a result the overall tax rate on personal income revolves around 36 percent instead of the usual 52 percent.

Legal aspects of establishing a Dutch office

Having a Dutch company in the framework of an international corporation provides both tax and legal benefits. Some important legal benefits are:

1) The legal system in the Netherlands has provisions for various entities to match the characteristics and needs of the planned business operations;

2) The Dutch Commercial Chamber (KvK) is very efficient and cooperative;

3) It only takes a day or two to obtain legalization from a Dutch Latin notary and a court-issued apostille;

4) It is easy to arrange the appointment of a local managing director, for example, to meet the subsistence requirements; and

5) In 2012 the laws on private limited companies (BVs) were thoroughly amended and currently they are a lot more flexible.

The corporate law in the Netherlands has provisions for entities both with and without a legal personality (i.e. both incorporated entities and partnerships/contractual entities).

The more commonly used entities without a legal personality include:

1) sole trader/sole proprietor/a one-man business (Eenmanszaak); (technically, sole proprietorships are not legal entities);

2) general partnership (Vennootschap onder firma or VOF);

3) professional/commercial partnership (Maatschap); and

4) limited partnership (Commanditaire vennootschap or CV.

The more commonly used entities with a legal personality include:

1) private company with limited liability (Besloten vennootschap or BV)

2) public company with limited liability (Naamloze vennootschap or NV)

3) cooperative association (Coöperatie or COOP); and

4) foundation (Stichting).

The choice of a legal entity depends on the type of business to be conducted. Owners of small businesses and freelancers usually establish sole proprietorships, while larger enterprises are incorporated as private companies with limited liability (BVs), public companies with limited liability (NVs) and limited partnerships (CVs).

After you decide to start a business, the first step is to register it at the Commercial Chamber which will include it in the Trade Registry. This procedure must take place during the period starting a week before your business becomes operational to a week after that.

Further details about the private company with limited liability (BV)

The private company with limited liability (Besloten Vennootschap or BV) with nominal capital split into shares is the most commonly used entity for business operations in the Netherlands. A BV has one or multiple shareholders and issues only registered shares. It can have one or several “incorporators” or subscribers who can be legal entities and/or natural persons. An entity or an individual, be it resident or foreign, can simultaneously be the sole incorporator and director representing the board of management.

Geographical features: Holland as an international commercial centre

Holland is an ideal strategic destination for businesses thanks to its connectivity. Companies established in the country can easily place their products and services on markets in the EU, Eastern and Central Europe, Africa and the Middle East. Holland is located in the western part of Europe and has common borders with Belgium (south) and Germany (east). To the west and to the north it borders the North Sea and its coastline is 451 km long. Holland is a small country with a territory of 41 526 square kilometres. Its economy is strongly dependent on international trade (more than 50% of the Gross Domestic Product is derived from foreign trade). The country is among the world’s top 10 exporting nations, which is quite an achievement for its size. Approximately 65 percent of all Dutch exports are destined for five countries: USA, the United Kingdom, Belgium, Germany and France.

More than 50% of all export and import in Holland consist of foods, machinery (mainly computers and parts) and chemical products. Many import goods (computers included) are actually destined for other countries and are re-exported largely unprocessed soon after their arrival in Holland. This situation is typical for big transportation and distribution hubs. As a matter of fact many millions of tonnes of North American and Asian goods arrive at Amsterdam or Rotterdam for distribution all over Europe. The role of Holland as an European gateway is also sustained by Schiphol Airport in Amsterdam – the fourth busiest and biggest airport on the continent servicing traffic of both goods and passengers. Most Dutch transportation companies have their bases of operation either in Rotterdam (with Rotterdam The Hague Airport) or close to Schiphol. Other major European airports, namely Düsseldorf and Frankfurt in Germany, Roissy in France and Brussels and Zaventem in Belgium are only several hours away. Furthermore Holland has an exceptional railroad network connecting important European capital cities, including London. The EU capital of Brussels is only a short ride away. Also, Rotterdam’s port is the biggest on the European continent. Until 12 years ago it was also the busiest port in the world, but was overtaken by Shanghai and Singapore. In 2012 it was the sixth busiest port in the world as regards tonnage of cargo per year.

Cost of labour

The living standards in Holland are relatively high and this is reflected by the average salary. In 2015 employers paid 2500 Euro/month to their employees and therefore the average cost of labour was 34.10 Euro/hour. All due taxes are levied at the source of income. The average work week is about 40 h.

The costs of labour in the different members of the EU vary widely. In 2015 the average pay per hour for the whole European Union was 25 Euro, and for the Eurozone the rate was 29.50 Euro. Therefore the costs of labour in the Netherlands are 16 percent higher compared to the average Eurozone value. Still, in 2015, five EU countries had higher labour costs than Holland. The average pay per hour in Denmark (41.30 Euro) and Belgium (39.10 Euro) is approximately 10 times higher compared to the value for Bulgaria (4.10 Euro). The labour in Belgium is more costly than in Luxembourg, the Netherlands, Sweden and France. Yet, the costs of labour in Lithuania and Romania are not much different than the cost in Bulgaria, even though the salaries in these 3 countries are on the rise.

As of 07/2015, the national minimum gross salary in Holland for employees aged 23 and older is 1507.80 Euro/month, i.e. 69.59 Euro/day. Based on 40 working hours per week, this equals 8.70 Euro/hour.

Amsterdam: The new European capital of finance

According to the writer James Stewart, a business columnist working at the NY Times, after Brexit Amsterdam is bound to become the new London thanks to its impressive architecture, top rated schools and exciting night life. Holland has been a global centre of commerce for centuries and so the country is traditionally tolerant to foreigners. Furthermore almost all Dutch residents speak English. The schools in Holland are considered the best on the European continent, with many opportunities for education in English. Amsterdam captivates with its architecture and offers attractive housing options, outstanding restaurants, picturesque views, theatrical and musical performances and an exciting night life. Its citizens have a tolerant, cosmopolitan attitude cultivated for centuries, ever since its emergence as a centre of global trade.

Thanks to the continuous efforts of the nation Holland is currently among the wealthiest states worldwide. The country’s strategic location on the North Sea coast and its rivers, bringing industrial and agricultural benefits have undoubtedly contributed to this success. Thanks to these geographical characteristics and the inherent work enthusiasm of its people, the Netherlands is now a great centre of commerce.

In addition, Holland has a well developed welfare state system ensuring that all the citizens share the prosperity of their homeland. The Dutch take great pride in their high living standards. The expenses associated with living, education, housing and culture are lower compared to most countries in Western Europe. The United Nations Sustainable Development Solutions Network surveys many people residing in various countries worldwide to prepare its annual World Happiness Report. As evident by its name, the report states which countries have the happiest populations. In 2018 Holland took the 6th place.

Cost of living

Similarly to many other countries in Europe, the living cost in Holland has increased with the adoption of the common currency, the Euro. A standard room costs 300 – 600 Euros/month, so it is a lot cheaper to settle in a non-urban area, than to live in a city like Amsterdam or The Hague.

The public transportation is comparatively cheap by EU standards. Most areas work with chip cards (“ov-chipkaart””) that can be used on trams, buses, metros and trains. In the city a single bus ticket costs approximately 2 Euro. A ticket for the train from Schiphol to the Central Station in Amsterdam costs about 4 Euro. A ticket Amsterdam – Utrecht is around 7.50 Euro. In contrast, taxi services are quite expensive. The usual starting cost is 7.50 Euro and the rates reach 2.20 Euro/km.

Please, do not hesitate to call our experts in taxation and incorporation. They will happily assist you with the procedures for starting your own business in Holland.

Foreigners residing in the Netherlands can either work for local businesses or establish their own companies. For the past few years people increasingly choose the second option, relying on the governmental support for start-ups.

One of the profitable businesses foreigners can establish in the Netherlands is shops. There are not many requirements to be fulfilled or licenses to be obtained. One significant advantage is the possibility to stock shops with quality products delivered from local manufacturers and producers. This is particularly convenient for low-cost consumer goods that are sold quickly.

Our local agents in company formation can assist you with the procedure for company registration with the aim to open a shop.

Registration of a shop in Holland

In order to open a shop, first you need to register your company at the Commercial Register. The procedure for company formation in the Netherlands requires:

- choosing a company name;

- selecting a form of business;

- registering the selected entity;

- registering with the Tax Administration;

- obtaining a social security registration;

- applying for a company account in a local bank, an additional merchant account is optional;

- obtaining the licenses necessary for operation.

As regards the licenses needed for opening a Dutch shop, the requirements vary depending on the offered products.

Licenses necessary for operating a Dutch shop

Of the permits necessary to open a shop in Holland, perhaps the most significant is called a market license. It allows both sole traders and companies to sell products on the Dutch market. This license is provided by the municipality of the area where the business operates.

In addition to the abovementioned market license, opening a Dutch shop implies certain measures for safety that must be considered by the business owners. The sold products need to be insured, and different contracts with the suppliers need to be signed. In particular cases, when selling imported products, the shop owners will have to obtain import permits.

If you need further information on registering a Dutch company, do not hesitate to get in touch with us. Our local consultants in company registration will assist you with the procedure for business incorporation. You can also check our guide on opening a Restaurant, Cafe or Hotel business in the Netherlands.

If you intend to start a business on the European continent, you have to choose a suitable country to begin with. Europe includes 44 countries (28 members of the EU) of various sizes, languages and levels of economic development. You might consider the Netherlands as a good place to establish your European business. The five main reasons why you should are listed below.

-

English will do everywhere

Regardless of the part of Holland you are in, the locals will speak basic English as a minimum. Your beginner’s attempts to speak Dutch will most likely result in replies in English. The widespread knowledge of the English language has multiple advantages, among which:

- Drafting agreements in English is common practice. You don’t have to translate your contracts in Dutch for them to be legally binding.

- If you employ local personnel or use the services of Dutch vendors, you will not encounter serious communication problems.

- You will not need to adapt your manuals or product packaging;

- The marketing slogans of your company can remain in English, though it may be appropriate to translate your other advertisements.

-

Short distances for travel

The big cities like the capital of Amsterdam, Utrecht, Den Hague and Rotterdam are an hour away from one another by car, at the most. The Randstad megalopolis hosts seven of the fifteen million people living in the country. Even the far-off regions or towns are no more than 3 hours away by car. Therefore you will be able to operate on the whole territory of the country from a single location.

-

Considerable spending power

Statistics show that in Holland the gross domestic product per capita rates among the highest worldwide. And, unlike in other top scoring countries, the distribution of income is relatively even. Therefore most Dutch residents have quite a bit of spending money.

-

Good opportunities online

The broadband penetration in the Netherlands rates among the highest worldwide due to the coaxial and phone networks covering the entire country. Dutch people shop readily online, while it is cheap and easy to arrange payments for the services and goods you offer. Consumers are not biased and more inclined to buy Dutch products: good deals always attract customers.

-

Setting up a company is easy

The last competitiveness ranking prepared by the International Institute for Management and Development rates the Netherlands 1st on the European continent and 4th in the world with respect to competitiveness. With the help of Intercompany Solutions, you can register your company within a few days. Small businesses need to meet few requirements and it is not obligatory to appoint an accountant or a local director. The rate of corporate income tax is twenty percent. You will also need to pay a fifteen percent withholding tax, but this could be settled with taxes on dividends covered by you elsewhere.

If you need further information on company establishment in Holland, please, get in touch with our qualified agents. If you are interested in starting a business in the Netherlands, you might also like our article with 5 ideas for opening a small Dutch business.

According to the legislation on the types of investment vehicles that can be registered in Holland, these structures may be established as investment companies or funds. Investors intending to go through the procedure for starting a fund can register their vehicles as closed- or open-ended forms of business.

Legal entities applicable for investment funds in the Netherlands

The Dutch legislation relating to investment funds includes various acts concerning the different regulated vehicles. To give an example, funds with a closed end are subject to Directive 2003/71/EC on the prospectus to be published when securities are offered to the public or admitted to trading, and are implemented in accordance with the EU legislation. Regardless of whether a fund has been established in a closed- or open-ended form or as a related vehicle, e.g. a start-up hedge fund, the Dutch laws prescribe the following five legal entities:

- private limited company (BV);

- public limited company (NV);

- cooperative;

- limited partnership;

- mutual fund (FGR).

Businessmen willing to open a Dutch fund also have the option to establish a variable capital investment company (BMVK). This entity acts as a fund for investments because its investors can set up umbrella funds in its structure. Still, in contrast to investment funds, a BMVK is not obliged to offer its stocks on the national market.

Corporate and non-corporate Dutch entities

The Dutch legal entities that can be used for investments belong to two general categories: corporate and non-corporate. The first group includes the BV, NV, cooperative and MBVK. The second features mutual funds and limited partnerships.

All these structures are taxed differently, in accordance with the system for taxation that covers them. The tax system in Holland allows legal entities open for investment funding to be established either as opaque or transparent. For opaque entities, the tax administration levies corporate tax with respect to capital gains and income.

Our company in the Netherlands can provide you with further information regarding the taxation of the structures listed above. Please, get in touch with our agents to receive detailed information on the legislation governing investment funds.

The procedures for appointment and dismissal of staff are partially covered by the Civil Code of the Netherlands and partially clarified by the judicial system. It is relatively easy to employ staff, but it may prove tricky to dismiss employees.

Employment contracts under Dutch law

The Dutch law on employment does not require a contract in written form. However, it is advisable to conclude written contracts with your employees to avoid discussions about the arrangements. It is good to start your employment contract with definitions of the most significant conditions for work.

The written employment contract also allows both the employer and the employee to include particular clauses, for example regarding non-competition, trial period, company secrecy, working hours, salary, bonus regulation, holidays, pension scheme, terms of termination, etc.

The contract for employment can be prepared in a language other than Dutch or English, but in such case, there is a risk of misinterpretation. Therefore a contract in one of those two languages is preferable.

If the hired employee is living and working in Holland, then the applicable law would be the Dutch one. In special cases, however, where the individual works in two or more countries, the provisions may be different. The particular circumstances will be determined by the governing law. The parties may need to consider the legislation of different countries.

In the Netherlands, it is advisable for employers to draft their contracts according to the local Dutch laws. Otherwise, some conditions or arrangements may prove to be invalid.

Agreements for employment in the country can be concluded for a particular or indefinite time period. However, fixed-term and open-ended contracts are subject to specific legislative provisions. Furthermore, the law is continually changing and therefore the agreement for employment needs to be revised regularly.

Dismissal of staff in the Netherlands

It may prove difficult to fire an employee by reason of various legal provisions related to dismissal.

First of all, you should have reasonable arguments in support of your decision to end the employment agreement. The law in the Netherlands mentions eight possible reasons, including economic circumstances, underperformance, serious misconduct, sick leave with a duration of more than 2 years and frequent illnesses.

The employment contract can be terminated via different routes. The easiest approach is to conclude a termination agreement ending the employment with mutual consent. During this process, the two parties often enter negotiations. You can also terminate the employment agreement by asking the Agency for Insurance of Employees (or UWV) to issue a permit for dismissal. This is a possible solution only in case the employee has been on a sick leave for 2 years or more or the job has become redundant because of technical, economic or organizational reasons. The third possibility is to seek contract dissolution in court due to shortcomings such as underperformance.

The UWV and the Court would not permit termination of an employment agreement if there is a prohibition for dismissal (e.g. during sick leave or pregnancy).

In the Netherlands, the dismissal procedure is heavily regulated. We are prepared to assist you in understanding the rules and applying them in your best interest.

In case you have questions on the mentioned topics, our Dutch office will be happy to give you answers and provide you with the ins- and outs of the Dutch workforce.